What is Economics at Its Core?

Ashvika Kotha

When people hear the word ‘economics,’ they assume that it is all about money; however, money is only one aspect of economics. Economics is the study of how people make decisions to allocate resources and how those decisions impact society. The most important concepts in economics, in my opinion, are scarcity, supply and demand, and economic equilibrium. There are two main branches in economics: microeconomics (individual choices) which deals with entities and their interaction with each other, and macroeconomics (aggregate outcomes) which manages the economy as a whole.

The term ‘scarcity’ alludes to a fundamental economic conundrum – discrepancy between finite resources and hypothetically unbounded wants. Scarcity, also known as paucity, is an economics term used to refer to a gap between availability of limited resources and the theoretical needs of people for such resources.

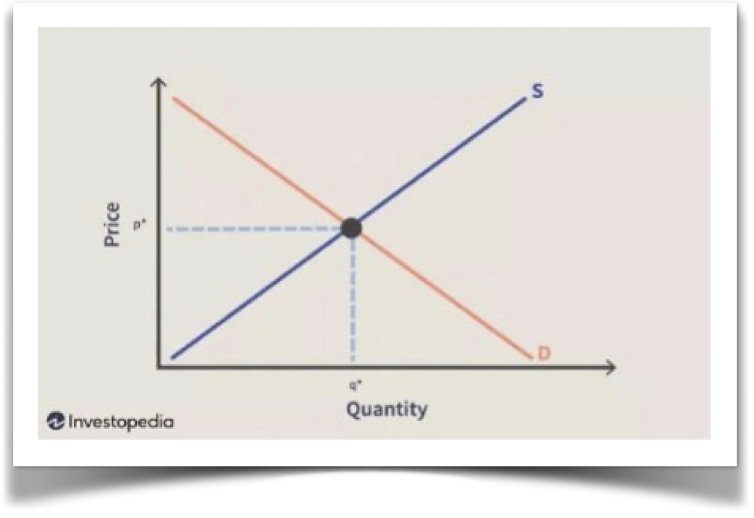

The quantity of a good (or service) that consumers are willing to buy at a specific price is known as demand. The quantity of an item that sellers are willing to deliver for a certain price is known as supply. According to the law of demand, if all other conditions are equal, fewer individuals will seek a good whose price is higher, because the opportunity cost of purchasing a good increases as its price rises. Customers buy less of a good when the price is higher; this enables them to allocate money to meeting other needs. The law of supply illustrates the amounts sold at a particular price; this implies that the quantity offered will increase as the price does. In practise, people’s willingness to supply and demand a good determines the market equilibrium – the price where the quantity of a good that people are willing to supply equals the quantity that people demand.

When the demand price is equal to the supply price, the amount produced has no tendency either to be increased or to be diminished; it is in equilibrium. In microeconomics, economic equilibrium may also be defined as the price at which supply equals demand for a product. Equilibrium can also refer to a similar state in macroeconomics, where aggregate supply and aggregate demand are in balance.

The law of demand and supply is true to its rules for most cases; however, some significant exceptions are there. For example, necessities, and luxury goods. Sir Robert Giffen came up and developed Giffen Goods which is exemplified by the Irish Potato Famine. This reversal of the law of demand saw the demand for potatoes increase as the price of potatoes increased. The idea behind a Veblen goods was made by economist Thorstein Veblen. This frequently occurs with luxurious goods, precious stones, and automobiles like Ferraris. An item’s value and worth are perceived to be greater when its expensive, and as a result, there is a greater demand for that good or service.

To conclude I think that economics at its core echoes what Thomas Sowell said, ‘the first lesson of economics is scarcity: there is never enough of anything to satisfy those who want it.’

This essay won Ashvika a partial Scholarship to attend summer programmes at the Universities of Oxford and Cambridge.

Related Posts

An Insight into the World of SAP Architecture

Rajiv Kaul In the ever-evolving realm of technology, the role of IT co

Book Review – The Midnight Gang

Adhya Raina I think The Midnight Gang is a really good book and here a

Creating Your Own Benchmarks

Amit Kotha, a stalwart banker, set up Beryllus Capital in March 2021 i

Coming of Light

Aadya Bakshi James lived in a perfect community. Everyone was ki

Its Not Rocket Science!

Palash Mattoo Rocket science and music theory have a few things in com

Actions Can Speak What Thousand Words Cannot

Dr Anita Sharma Raina MBBS; FRCGP; DFRSH; Diabetes (Dip); MSc (Edu) It